Blog Article

LA multifamily investors: Understand why mortgage rates remain in the mid-6% range despite Fed rate cuts. Learn how the 10-year Treasury yield impacts your financing costs.

Kenny Stevens Team

Stay Updated on Exclusive Opportunities & Off-Market Deals

Los Angeles Multifamily Mortgage Rates 2024: Why Rates Haven't Budged Despite Fed Cuts

Los Angeles Multifamily Mortgage Rates 2024: Why Rates Haven't Budged Despite Fed Cuts

The Fed cuts made headlines, but why are rates still high?

In recent months, the Federal Reserve implemented two interest rate cuts as a strategic attempt to stimulate economic activity. Yet despite these moves, mortgage rates remain stubbornly fixed in the mid-6% range. For multifamily investors in Los Angeles, this disconnect is frustrating and confusing.

The answer lies in a fundamental misunderstanding about how mortgage rates work. Although the Federal Reserve influences the broader financial landscape, it doesn't directly set mortgage rates. Instead, a complex interplay between investor sentiment and the 10-year Treasury yield dictates where mortgage rates land. As Brookings notes, "The Fed's rate cuts signal monetary policy shifts, but mortgage rates are tied to broader market dynamics."

This distinction is crucial for understanding Los Angeles multifamily mortgage rates 2024.

How the Federal Reserve Actually Influences Mortgage Rates

The Federal Reserve holds significant influence over the economy by adjusting the federal funds rate, which is the cost banks charge each other for overnight loans. These adjustments ripple through the financial system, indirectly impacting consumer interest rates for loans and credit cards. However, mortgage rates are not directly tied to the Fed's benchmark rate.

As NPR highlights, "The Fed's rate decisions can set the tone, but mortgage rates have their own rhythm." Mortgage rates instead follow broader market trends, with the 10-year Treasury yield serving as a critical benchmark. This is an important distinction for multifamily property owners trying to time their financing decisions.

Why Los Angeles Multifamily Mortgage Rates Remain Elevated

Despite the Fed's efforts to lower rates, several factors keep Los Angeles multifamily mortgage rates elevated in 2024:

High 10-Year Treasury Yields

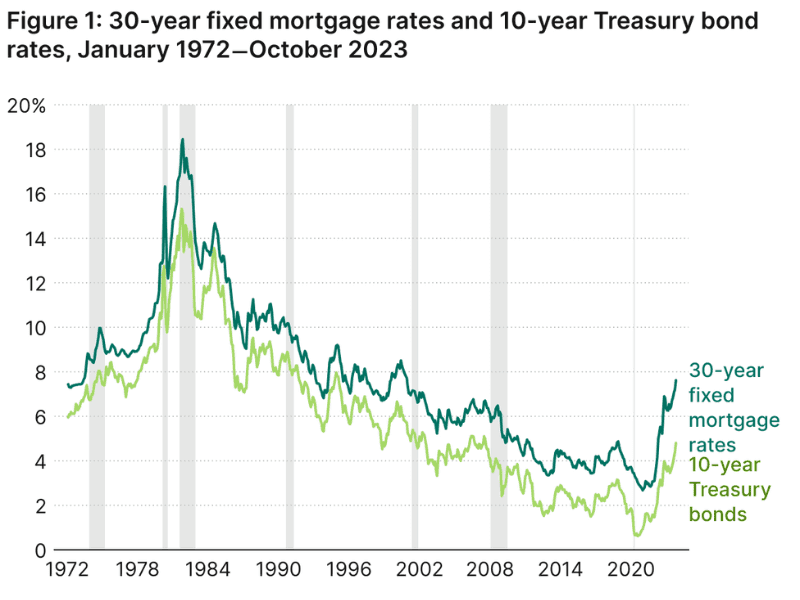

Mortgage rates are closely tied to the 10-year Treasury yield, which has remained elevated due to reduced investor demand for bonds. When bond demand falls, yields rise. Higher yields lead to increased borrowing costs for lenders, which are passed along as higher mortgage rates. This is the primary driver of where Los Angeles multifamily mortgage rates currently sit.

Risk Premiums in Uncertain Markets

Lenders incorporate higher risk premiums when markets are uncertain. Given the volatility in bond markets and the possibility of future inflation spikes, lenders remain cautious. They build these premiums directly into mortgage rates, making financing more expensive for multifamily investors.

Persistent Market Uncertainty

Investor skepticism about inflation and global economic stability has driven up yields on government bonds, including the 10-year Treasury note. This uncertainty translates directly into higher borrowing costs for multifamily properties.

Resilient Economic Activity

Despite some signs of cooling, parts of the economy remain resilient, creating upward pressure on rates. The labor market, for example, has shown continued strength, with employment remaining near historic lows. This economic resilience keeps the Fed from cutting rates more aggressively, which in turn keeps Los Angeles multifamily mortgage rates elevated.

Understanding the 10-Year Treasury Yield and Its Impact on Your Financing

The 10-year Treasury yield is often referred to as a bellwether for the economy. According to CBS News, "The 10-year Treasury yield is a key metric for mortgage lenders, as it reflects long-term economic sentiment." For multifamily investors, understanding this relationship is essential.

When demand for Treasury bonds is high, yields fall, typically dragging mortgage rates down with them. Conversely, when investors pull away from Treasury bonds, yields rise, pushing mortgage rates higher. Mortgage rates typically move in tandem with the 10-year Treasury yield because both instruments are influenced by similar economic factors: inflation expectations, employment data, and overall market sentiment.

For Los Angeles multifamily investors, this means monitoring Treasury yields is just as important as watching Fed announcements. The 10-year Treasury often provides a better indicator of where multifamily mortgage rates are headed than Fed rate decisions alone.

What This Means for Los Angeles Multifamily Investors

Navigating a high-rate environment can feel daunting, but opportunities are still out there. Understanding why Los Angeles multifamily mortgage rates 2024 remain elevated helps you make better financing decisions.

If you're considering financing or refinancing a multifamily property, focus on the fundamentals: strong cash flow, quality assets in prime locations, and realistic return projections. In a higher-rate environment, these factors matter more than ever. Properties that can generate strong returns despite elevated borrowing costs will continue to attract investor interest.

The key is not to wait for rates to drop to perfect levels. Instead, evaluate each opportunity on its own merits. Some multifamily deals still make sense at current rates, particularly if you're acquiring quality assets below replacement cost or in markets with strong rent growth potential.

The Bottom Line

While the Federal Reserve's rate cuts make headlines, Los Angeles multifamily mortgage rates 2024 follow a different path. The 10-year Treasury yield, investor sentiment, and broader market dynamics have far more influence on your financing costs than the Fed's benchmark rate. Understanding this distinction helps you navigate the current market more effectively.

The Kenny Stevens Team stays current on market dynamics and how they impact multifamily financing in Los Angeles. Contact us to discuss your financing options and how current mortgage rates affect your multifamily investment strategy.

Explore Related Posts for Deeper Insights

The Stevens Difference

Kenny Stevens Team brings 25+ years of Los Angeles multifamily experience, with $2.75B+ in LA apartment sales across 675+ closed transactions.

37

COMBINED YEARS OF EXPERIENCE

Selling and trading Los Angeles multifamily real estate

KST

AVERAGE

Sold price to listed price